Insights

Periodic insights from our Investment and Private Client Teams on a broad range of investment and advice-related topics

Published by the Private Client Team at KJ Harrison Investors

The global pandemic is clearly not over, but perhaps we can now safely say that the dark clouds of the COVID-19 environment are dissipating. The development and deployment of effective vaccines, social distancing practices, nascent herd immunity and better weather all seem to be setting the stage for the return to something like “normal” life over the next few months. That is certainly good news for individuals, businesses and the broader economy. As the world reopens, we can expect a surge in economic activity, the return of inflation, and a wave of investor and consumer euphoria.

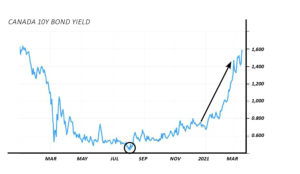

Yet for investors, the post-COVID reflation is not likely to be uniformly good news, because it could well wreak havoc on the portion of their portfolio that is supposed to be the safest: fixed income. In fact, the havoc seems to have already begun. As financial markets anticipate recovery, interest rates are rising. From the start of the year through March 10th, the Government of Canada 10-year bond yield rose by more than 60 basis points and more than doubled from its low in July 2020. This sharp increase has adversely impacted traditional fixed income across the spectrum of bond classes, because of the inverse relationship between yield and price. The “great reflation” presents heightened risks to investors who are following the traditional 60% equities/40% bonds approach in their portfolios as there is risk to rates continuing to rise. Quite suddenly, the “safe” part of that typical portfolio – bonds – seems not so safe anymore. The challenge for fixed-income investors now is this: How can they continue to generate income while mitigating interest rate risk?

KJ Harrison offers its clients two potential solutions in the KJH Credit Fund and the KJH Senior Loan Fund¹.

The KJH Credit Fund, focused on Canadian investment-grade corporate fixed-income securities, employs a hedging strategy with the objective of maximizing risk-adjusted returns and minimizing interest rate risk. The KJH Senior Loan Fund, meanwhile, seeks to generate stable income while minimizing long-term volatility, by focusing on senior bank loans and non-investment grade corporate borrowers. While both of these strategies differ, they share a common goal: to effectively insulate fixed-income allocations from rising interest rates.

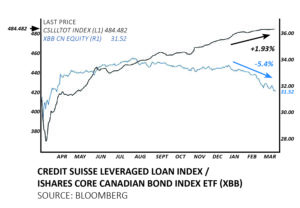

Before we discuss how and why, let us consider the risks that reflation poses to traditional bond allocations. The 2021 year-to-date total return for the FTSE Canada Universe Bond Index, which comprises government and investment-grade corporate bonds, declined by around 5.4%. The adverse impact of rising rates has been even more severe for longer-duration bonds (10+ years to maturity): declines to the end of February were 7.1%. Those are big downside numbers, to which fixed-income investors are simply not accustomed. If rates continue to rise, they threaten to eradicate the returns bond investors have enjoyed through a years-long bull market.

The bigger picture is that interest rates have been held low, which has created a huge challenge in particular for institutional investors who, because of regulation or fiduciary responsibility, must maintain exposure to fixed income. Yields have been so low that bonds have largely not generated the kind of steady income that would allow investors to take on more risk in their equity allocations. As we are seeing now, low rates create another problem: even a relatively small increase in yield has a large impact on price. For example, if the yield on a 10-year Canada bond rises from 1% to 2%, its price will decline by around 8%. An investor in that bond will experience both a negative real return and rather extreme price volatility.

In our view, these realities should encourage investors to consider alternatives to a 40% traditional bond allocation within a balanced portfolio. Among those is the KJH Senior Loan Fund, which predominantly invests directly in U.S.- syndicated, first-priority, secured term loans to non-investment-grade companies. While not well known among Canadian investors, senior loans are a huge asset class globally, totalling about US$1.4 trillion. They are also one of the very few asset classes that can generate positive real return simply from their coupon payments (as opposed to bond returns, most of which has been generated by capital appreciation).

Importantly, the coupons for senior loans float, and are largely tied to the overnight London Interbank Offering Rate, or LIBOR, which in turn is correlated with the U.S. Federal Reserve funds rate. Given that the Fed has signalled it intends to maintain near-zero rates until 2023, we do not envision the LIBOR rising anytime soon, suggesting relatively low volatility for senior loans. The asset class also offers low correlation to the U.S. Aggregate Bond Index, and senior loans can generate steady returns whether bond yields go up or down. The average duration of the KJH Senior Loan Fund is extremely short – on the order of 0.25 years, compared with the FTSE Canada Universe Bond Index average duration of more than eight years. (Shorter-duration instruments are less sensitive to changes in interest rates than longer-duration ones.)

In these ways, the KJH Senior Loan Fund offers low correlation to traditional fixed income, low volatility, low duration risk and near-zero interest rate risk. Credit risk is also mitigated, as the loans in the portfolio are senior, meaning in the event of bankruptcy they are resolved first (before other instruments such as high-yield bonds); the Fund seeks to invest in well-known companies with a stable credit outlook. Based on historical data, those factors suggest that allocating 10% to 15% of fixed income exposure to senior loans can significantly increase the risk-adjusted return of the overall fixed-income portfolio. The recent rise in interest rates presents a test case for this expectation: the benchmark Credit Suisse Leveraged Loan Index returned 1.93% between January 1st and March 5th 2021 (see chart above).

The KJH Credit Fund similarly seeks to mitigate interest rate and duration risk with low correlation to wider bond and equity markets, but it employs a very different strategy. The Fund largely generates return from the yield differential between investment-grade Canadian corporate bonds and government of Canada bonds. It does that by selling a similar-duration government bond for every corporate bond it buys – a hedging strategy that eliminates interest rate risk – and it leverages exposure to short-duration corporates, minimizing volatility in the spread and mitigating duration risk. The Fund also generates returns through capital appreciation when the spread between corporate and government bonds compresses.

Given that its hedging strategy results in a net zero capital outlay, the Fund invests cash in short-term moneymarket instruments (with an average duration of about a month) and new debt issues, which offer the potential for price appreciation after distribution. Finally, the managers seek to take advantage of short-term trading opportunities and potential mispricing of debt instruments in the corporate bond market. As with any corporate debt, the Fund’s strategy does invoke credit risk; however, corporate default rates are expected to decline as the Canadian and global economies recover.

Although their approaches differ, the KJH Senior Loan Fund and KJH Credit Fund similarly offer the valuable portfolio characteristics of low volatility, low correlations to other asset classes, fixed income exposure, and capital preservation. In today’s reflationary environment, these funds represent dynamic, creative approaches to the primary challenges that the post-COVID recovery – as welcome as it is – presents. In our view, investors would do well to consider how such strategies might improve risk-adjusted returns within a diversified portfolio – even if that means rethinking the traditional 60/40, as we believe they should.

1 – YTM Capital Asset Management Ltd. is the Portfolio Manager for KJH Credit Fund and Wellington Square Capital Partners Inc. is the Portfolio Manager for KJH Senior Loan Fund.